In the previous installments, we first examined the physical and geopolitical causes of techflation (the perfect storm), before detailing its immediate consequences on prices, the mobile industry, and the fragmentation of the internet (the reality shock). In this third and final part, we look ahead to the coming decade to understand how to survive and navigate this new world.

Long-Term Implications: Toward a New Technological Social Contract

Looking out five to fifteen years, techflation and today’s geopolitical crises no longer appear as mere bumps in the road, but as the catalysts for a civilizational shift. The very foundations of our relationship with technology, industry, and democracy are being redrawn.

Toward a New Global Industrial Geography

The sweeping reindustrialization movement, long dismissed as wishful thinking or hollow political rhetoric, is becoming a tangible reality, driven by sheer survival instinct. Europe and the United States have learned, at great cost, that outsourcing the production of their critical infrastructure to distant countries with sometimes competing interests was a major strategic blunder.

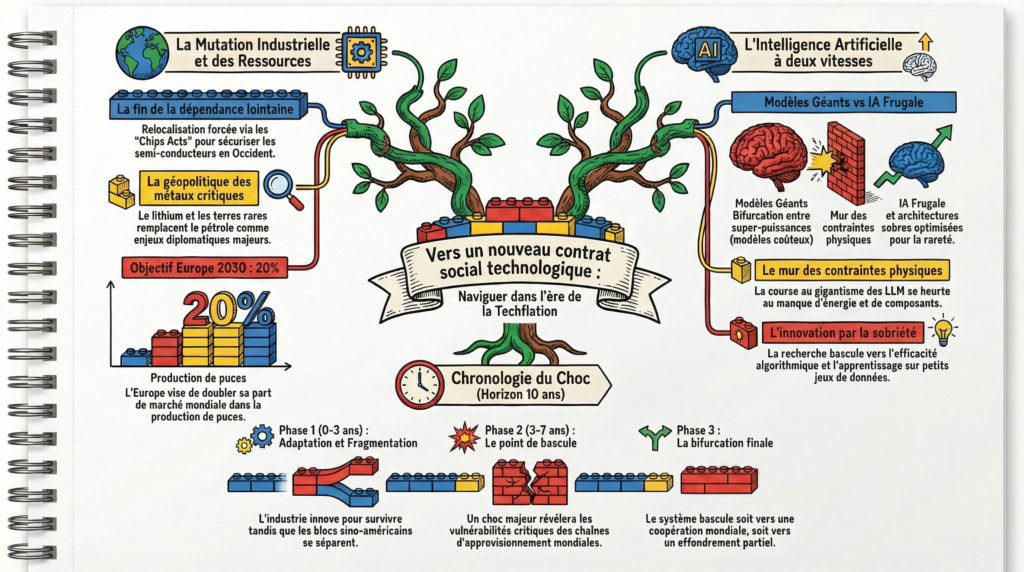

In the United States, the CHIPS and Science Act, backed by tens of billions of dollars in subsidies, aims to bring semiconductor manufacturing back to American soil. In Europe, the European Chips Act pursues a similar goal: to double the continent’s share of global chip production by 2030, targeting 20%. Enormous projects are breaking ground, such as Intel’s mega-factory in Magdeburg and TSMC’s facility in Dresden, Germany.

That said, this shift toward a new industrial geography will be neither fast nor painless. The human and economic cost of this forced relocation will be enormous. Rebuilding complex industrial ecosystems requires not just factories, but entire networks of subcontractors, massive energy infrastructure, and above all, a highly skilled workforce that is sorely lacking in the West today. The bill for this reindustrialization will inevitably be picked up by taxpayers, through public subsidies, and by consumers, through higher prices. That is the price of resilience.

At the same time, a new geopolitics of resources is taking shape. Critical raw materials (lithium, cobalt, rare earth elements, tungsten, and others) have become the new oil of the 21st century. The energy transition and the digital revolution rest entirely on these metals, whose extraction and refining are today largely dominated by China. Securing access to these supplies will shape diplomatic alliances and military strategies for decades to come, turning mining nations in Africa and South America into major geopolitical stakes.

AI in a World of Scarcity: Slowdown or Bifurcation?

The current trajectory of artificial intelligence, built on an unchecked race toward ever-larger models (the so-called LLMs, or Large Language Models), will inevitably collide with the wall of physical constraints. Training increasingly vast models requires exponentially growing amounts of computing power, memory, and energy. In a world shaped by techflation and component scarcity, this headlong rush becomes unsustainable.

We are therefore heading toward a major bifurcation in AI development. On one side, a handful of tech superpowers, American and Chinese, will continue developing titanic frontier models, reserved for critical applications or clients able to pay enormous sums to access them. On the other, necessity will drive the emergence of far more frugal AI architectures, optimized to operate with limited resources.

Research will pivot massively toward algorithmic efficiency, model compression, and learning from smaller but higher-quality datasets. The goal will no longer be to build an all-knowing AI, but specialized systems capable of performing specific tasks with a minimal energy and material footprint.

The inherent risk in this evolution is the emergence of a two-tier artificial intelligence. Wealthy nations and large multinationals will have access to the highest-performing models, capable of generating massive productivity gains and disruptive innovation. Developing countries and small businesses will be left with second-rate models, less capable and potentially already obsolete. Techflation could thus dramatically amplify global economic inequality, turning the digital divide into an unbridgeable chasm.

Rethinking the Contract Between Tech and Democracy

The current crisis also exposes the limits of Big Tech’s development model. For years, these companies have accumulated financial, technological, and political power that rivals, and in some cases surpasses, that of many sovereign states. They have dictated the rules of the game, imposed their standards, and evaded any meaningful regulation, all in the name of innovation and free enterprise.

Today, as their strategic choices (such as concentrating production in Asia or hoarding resources for AI) threaten global economic stability, the question of their accountability is being raised with fresh urgency. When a private company can, through its investment decisions, drain the global memory market or paralyze entire sectors of the economy, it can no longer be treated as a simple commercial player. It becomes critical infrastructure, whose governance must incorporate the public interest.

There is a pressing need to rethink the social contract between technology and democracy. This means far stricter regulation of tech monopolies, not just on competition and data protection, but on the management of critical resources. Should allocation quotas be introduced for essential components, such as memory or advanced processors, to prevent them from being cornered by a small number of players? Should certain cloud infrastructures be treated as global public goods, subject to rules of neutrality and equitable access?

These dizzying questions call for the reconstruction of some form of global digital common good, a space where technology is no longer merely a tool of geopolitical domination or profit maximization, but an instrument in service of collective resilience and human progress. The task is immense, but techflation reminds us brutally that the status quo is no longer an option.

Possible Scenarios for the Coming Decade

Faced with these major uncertainties, several trajectories are taking shape for the future of the digital economy. History is not yet written, and the path we take will depend on the political and industrial choices made in the years ahead.

Scenario 1: Lasting Fragmentation (The Absolute Splinternet) In this scenario, geopolitical tensions continue to escalate. The world splits definitively into hermetically sealed technological blocs, led by the United States and China, with Europe attempting to maintain an illusory third way. Supply chains are entirely duplicated, causing a lasting explosion in costs, and techflation becomes the norm. Innovation slows, hampered by the absence of common standards and the restriction of the flow of talent and ideas. The global internet as we know it disappears, replaced by incompatible regional networks under tight state surveillance.

Scenario 2: Shock and Recovery (Forced Cooperation) A major crisis, for instance an open conflict over Taiwan or a sudden collapse of the semiconductor supply chain, delivers a worldwide electroshock. Faced with the prospect of global economic collapse, the great powers are compelled to sit down at the negotiating table. A new international treaty, a kind of “Digital Bretton Woods,” is signed. It establishes clear rules for sharing critical resources, securing supply routes, and regulating artificial intelligence. Techflation is brought under control through global coordination of industrial investment.

Scenario 3: Silent Adaptation (Resilience Through Innovation) The tech industry proves its extraordinary capacity for adaptation. In the face of material scarcity and rising costs, innovation pivots massively toward efficiency. New substitute materials are discovered to replace helium or rare earths. AI architectures become radically more frugal. The recycling of electronic components (the circular economy of tech) becomes a major industry, reducing dependence on mining extraction. Techflation acts as a Darwinian spur, forcing the ecosystem to become more robust and sustainable, without any dramatic visible geopolitical rupture.

Scenario 4: Partial Collapse (Systemic Crisis) Accumulated vulnerabilities finally give way. A succession of shocks (wars, climate disasters affecting key production zones, massive cyberattacks) causes the simultaneous breakdown of several critical supply chains. Entire segments of the digital economy grind to a halt. Hardware prices explode to the point of becoming unaffordable for the majority of the world’s population. Non-tech companies, unable to finance their digital transition, go bankrupt en masse. This worst-case scenario would see a significant technological regression, forcing societies to relearn how to function without the permanent support of digital tools.

From Probability to Sequence: A Systemic Reading

These four trajectories, while distinct, lack a clear hierarchy when viewed as a simple multiple-choice menu. To truly understand the dynamics of techflation, one must move beyond this static vision and adopt a probabilistic, sequential reading. In reality, these scenarios are not mutually exclusive; they unfold over time. The OECD has even begun quantifying these macroeconomic risks: in a severe energy shock scenario, the organization projects an impact of -0.5% on global GDP and +0.9% on inflation in the second year, while an early resolution of conflicts would bring a GDP gain of +0.3% and an inflation reduction of -0.7% [26]. These figures put the scale of the disruptions into perspective.

Silent adaptation is inevitable in the short term. Not because it is the most desirable outcome, but because it reflects the systemic reflex of markets. In the face of exploding costs, substitutes emerge, players innovate, and business models reorganize. This process is already underway. In parallel, the Absolute Splinternet is establishing itself as the dominant structural trend. The Sino-American decoupling, the fragmentation of supply chains, and the divergence of technological standards form the backdrop against which everything else plays out [18]. These two dynamics coexist: silent adaptation slows fragmentation, but does not stop it.

Forced cooperation, for its part, requires extremely precise conditions. Recent history, from the 2008 financial crisis to the Covid-19 pandemic, shows that global shocks tend to produce more national retrenchment than lasting cooperation [19]. For a “Digital Bretton Woods” to materialize, a shock violent enough to compel the great powers to reach an agreement would be needed, without triggering a total collapse [20]. That is a particularly narrow window of opportunity.

Finally, partial collapse represents what complex systems theorists call “fat tail” risk. In a linear model, this scenario seems unlikely. Yet, as Nassim Nicholas Taleb has theorized, hyper-connected, globalized systems accumulate invisible vulnerabilities that make cascading failures far more plausible than our habitual ways of thinking would suggest [21].

The Crisis Timeline

This hierarchy of probabilities maps onto a temporal progression in three distinct phases.

Phase 1: The Immediate Present (0 to 3 years) We are currently in a phase where silent adaptation and geopolitical fragmentation are unfolding simultaneously. Industry innovates and substitutes to survive, while decoupling deepens in the background. The system’s shock absorbers are still operating at full capacity.

Phase 2: The Tipping Point (3 to 7 years) If technological adaptation fails to keep pace with the speed of fragmentation, the system will reach a critical threshold of fragility. A major shock, such as an open conflict over Taiwan or the simultaneous breakdown of several supply chains, will then become the moment of truth, acting as a revealer of the accumulated vulnerabilities.

Phase 3: The Final Bifurcation That triggering shock will inevitably lead to one of two extreme outcomes, depending on the collective response of states. If governments react with sufficient clarity and speed, the crisis will give birth to forced cooperation and a new global governance framework. If, on the contrary, the shock exceeds institutional response capacity, or if geopolitical tensions prevent any coordination, the system will tip toward partial collapse.

What makes this reading particularly sobering is that it confirms the systemic nature of the problem. Fragile systems do not choose their crises; they are overtaken by them once all the shock absorbers have been exhausted one by one. Adaptation and fragmentation are our current buffers. Cooperation or collapse is what awaits us at the end of the road.

Learning to Navigate the World That Comes Next

Techflation is not a passing misfortune; it is the symptom of a change of era. The world of technological abundance, frictionless globalization, and the inexorable march of Moore’s Law is behind us. We are entering the age of scarcity, geopolitical friction, and physical constraint.

Faced with this new reality, collective denial is our worst enemy. Every actor must urgently grasp the scale of the disruption underway and adapt their strategy accordingly.

For states, and for Europe in particular, this is the moment for a strategic awakening. Digital sovereignty can no longer be a mere talking point in political speeches; it must become the central axis of industrial and defense policy. That means sustained, long-term investment to rebuild local production capacity, master critical technologies such as frugal AI and sovereign cloud, and secure access to raw materials. That is the price, and the only price, of avoiding permanent vassalization.

For businesses, the paradigm shift is equally abrupt. Technology can no longer be treated as a cheap commodity to be consumed without thought. Boards and executive teams must integrate geopolitical risk and techflation into their business models. That means ruthlessly auditing digital supply chains, diversifying suppliers, repatriating critical data to controlled infrastructure, and favoring resilient, resource-efficient technology solutions over the siren call of the latest overpriced innovations. Agility and frugality will become the watchwords of economic survival.

Finally, for us, citizens and consumers, this is about rethinking our relationship with technology. We must accept that the frenetic cycle of replacing our electronic devices is no longer sustainable, either ecologically or economically. We will need to learn to make our equipment last, to prioritize repair and the second-hand market, and to demand that our leaders protect our rights and our data against the appetite of digital giants.

Techflation is not the end of technology. It is the end of a debt we took on without realizing it, a decade of digital comfort built on geopolitical and physical foundations we chose not to examine. OECD projections for 2026 have since confirmed this new macroeconomic reality, with inflation revised upward to 4.0% for the G20 (+1.2 points) and 4.2% for the United States, while global growth would plateau at 2.9% [26]. Techflation is now a tangible, quantified, and enduring phenomenon.

The grief we refused to acknowledge at the start of this story is going to be forced upon us. Brutally. The question is no longer whether the world as it was will disappear. It is already disappearing, right before our eyes, while we keep on scrolling.

You have read this article to the end. You now know what most of your leaders, shareholders, and suppliers are pretending not to see. That knowledge is a responsibility.

So ask yourself one question, the only one that really matters: when the bifurcation comes, and it will come, on which side of history will you have chosen to stand? Among those who knew and did nothing, or among those who, in their own way, refused to let inaction be an option?

In a system as fragile as the one we have just described, not choosing is already a choice. Those who come after us will judge not so much what happened, but what we did once we knew.

References

[18] Nocetti, Julien. “A Splintered Internet? Internet Fragmentation and the Geopolitics of Digital Technology”. Ifri, February 2024. https://www.ifri.org/sites/default/files/migrated_files/documents/atoms/files/ifri_nocetti_internet_fragmentation_february_2024.pdf

[19] Jaax, Alexander, Sébastien Miroudot, and Elisabeth van Lieshout. “Deglobalisation? The Reorganisation of Global Value Chains in a Changing World”. OECD Trade Policy Paper No. 272. OECD, April 2023. https://www.oecd.org/content/dam/oecd/en/publications/reports/2023/04/deglobalisation-the-reorganisation-of-global-value-chains-in-a-changing-world_324dfabd/b15b74fe-en.pdf

[20] Medhora, Rohinton P., and Taylor Owen. “A Post-COVID-19 Digital Bretton Woods”. Project Syndicate / CIGI, April 2020. https://www.cigionline.org/articles/post-covid-19-digital-bretton-woods/

[21] Taleb, Nassim Nicholas. Statistical Consequences of Fat Tails: Real World Preasymptotics, Epistemology, and Applications. STEM Academic Press, 2020.

[26] OECD. “OECD Economic Outlook, Interim Report March 2026: Testing Resilience”. March 2026.