This dossier has been structured into three complementary parts, each exploring a different facet of the transformation now underway. They will be published every Tuesday, one episode per week, to allow time to fully grasp the mechanisms at play and their concrete consequences.

The old world is gone, and no one has yet mourned it

There was a time, not so long ago, when technology seemed to float above earthly constraints. We had come to believe in a kind of everyday magic. One click was enough to order a smartphone assembled on the other side of the world, another to store thousands of photos in a “cloud” we imagined as immaterial, a final one to query an artificial intelligence capable of digesting the entirety of human knowledge in seconds. This seamless flow, almost miraculous, rested on an implicit promise, that of a benign globalization, pacified by trade, where borders faded before the absolute efficiency of supply chains.

Today, that illusion has cracked from every angle. The old world is gone, and yet, collectively, we refuse to grieve it.

For decades, the tech giants lulled us into complacency. They sold us the idea that their infrastructures were inherently resilient, that geopolitics belonged to the past, or at least that it had nothing to do with Silicon Valley. Apple invested hundreds of billions of dollars in China, training tens of millions of workers, building entire cities around its factories, convinced that economic interdependence would prevent any conflict [7]. Microsoft, Google and Amazon deployed their data centers across Europe, presenting themselves not as commercial companies, but as the natural pillars of an unbreakable Atlantic alliance.

But the physical reality of the world is now taking its revenge on the supposed immateriality of the digital realm. Geopolitical and technological crises can no longer be read separately. They have become two sides of the same coin. When a drone strikes a gas facility in the Middle East, it is no longer just the price at the pump that is at risk, it is humanity’s very ability to manufacture the chips that power our hospitals, our cars and our artificial intelligences [1]. When tensions flare in the Black Sea or the Red Sea, it is the rare metals and maritime routes essential to our servers that are held hostage [8].

It is in this context of historical upheaval that a new phenomenon is emerging, subtle and profound: techflation.

It would be tempting to reduce techflation to a simple rise in the price of hardware or software subscriptions. That would be a major analytical mistake. Techflation is not a temporary fever caused by a short-term imbalance between supply and demand. It is a structural reshaping of the global digital economy. It marks the precise moment when technology ceases to be a deflationary force, one that made everything cheaper and more accessible year after year, and becomes instead a scarce, costly and fiercely contested resource.

We are entering an era where computing power, memory and access to the cloud will become markers of wealth and sovereignty. An era where companies will have to choose between paying exorbitant costs to maintain their infrastructures or fundamentally rethinking their relationship with technology. An era, finally, where states that failed to build their own digital independence will be reduced to the status of mere vassals, forced to pay a technological tribute just to operate.

To understand how we got here, and more importantly how to navigate this new world, we need to dive into the invisible workings of this global machine that is beginning to stall. We need to look beyond the smooth screens of our phones and see the factories, gas pipelines, mines and submarine cables. Because it is there, in mud, gas and metal, that the future of our digital world is now being decided.

The anatomy of a perfect storm

To grasp the scale of the shock ahead, one must first understand that the global digital economy is a house of cards of staggering complexity. Every component in your computer has likely circled the globe twice before reaching your desk. This hyper-specialization drove costs down dramatically, but it also created single points of failure. Today, several of these points are collapsing simultaneously.

Wars as economic catalysts

Geopolitics has abruptly entered the boardrooms of technology companies. Modern conflicts are no longer limited to territorial disputes, they are redrawing the fault lines of global supply chains.

Take the situation in the Middle East. Public attention naturally focuses on oil and gas prices, which makes sense for economies historically dependent on hydrocarbons. The OECD notes that exports passing through the Strait of Hormuz accounted for “around 20 percent of global production in 2025 and 25 percent of global seaborne oil trade”, while for liquefied natural gas, “around 93 percent of Qatar’s exports and 96 percent of those from the United Arab Emirates passed through the strait, representing nearly one fifth of global LNG trade” [26]. But deep within the industry, concern is shifting toward far more obscure elements. Tensions between Iran, the United States and Israel have turned these vital maritime routes, such as the Strait of Hormuz and the Red Sea, into high-risk zones. Yet these same arteries also carry electronic components between Asia and Europe.

Further north, the war between Russia and Ukraine exposed the extreme fragility of critical material supplies. Before the conflict, Ukraine produced around half of the world’s neon, a gas essential for the lasers used to engrave semiconductor circuits [8]. Although the industry has since adapted by building inventories and diversifying sources, the shock was profound. It demonstrated that access to vital resources such as palladium, of which Russia controlled 40 percent of the market, titanium or platinum [9], would never again be guaranteed or cheap. The lesson is clear: resilience comes at a cost, and that cost spreads across the entire value chain.

These conflicts act as revelations. They show that technology is not detached from the ground. It depends on physical resources located in unstable regions. And among those resources, one stands out as a perfect illustration of our collective blindness.

Helium, the symbol of a dependency we refused to see

When you think of helium, you probably imagine birthday balloons or the high-pitched voice it produces when inhaled. Yet this gas is one of the invisible pillars of modern civilization. It is irreplaceable, and no substitute exists for its most critical industrial uses.

The global geography of helium is alarmingly fragile. It is a byproduct of natural gas liquefaction. Qatar, sitting on the largest natural gas field in the world, alone produces about 30 percent of global helium in its massive Ras Laffan complex [1]. This dependence is confirmed by the OECD in its March 2026 report, which highlights that the Middle East produces “more than one third of global helium supply and more than two thirds of bromine supply, both important for industrial supply chains, including semiconductors and memory chips” [26]. The United States produces around 35 percent, with Algeria and Russia sharing the remainder.

In early March 2026, following Iranian strikes, Qatar’s national company declared force majeure, abruptly halting exports [1]. Overnight, nearly one third of the global supply vanished. Spot market prices doubled within weeks, and experts estimate that it could take months, even years if facilities are severely damaged, to return to normal [1] [6].

The consequences are staggering, because helium is everywhere. In the medical field, more than 14,000 MRI scanners worldwide rely on liquid helium to cool their superconducting magnets to near absolute zero. In aerospace, companies like SpaceX use it to pressurize rocket fuel tanks.

But it is in the semiconductor industry that the crisis is most acute. Manufacturing an electronic chip, such as the GPUs powering artificial intelligence, requires hundreds of nanometer-scale engraving steps. Each of these steps generates intense heat that must be dissipated instantly. Only helium, thanks to its exceptional thermal properties, can provide this level of cooling precision [1].

South Korea, home to giants like Samsung and SK Hynix, which control 70 percent of the global memory market, imports nearly 65 percent of its helium from Qatar [5]. Taiwan, where TSMC produces the world’s most advanced chips, faces a similar situation. These countries suddenly find themselves at the mercy of a conflict that does not directly involve them, illustrating the madness of an excessively globalized supply chain.

The memory crisis, when artificial intelligence devours its own industry

As if geopolitical shocks and raw material shortages were not enough, the tech industry has generated its own internal crisis, driven by excessive ambition. It is the story of an unprecedented cannibalization, where the race for artificial intelligence is draining the global component market.

At the heart of this storm lies DRAM memory, an essential component found in every electronic device, from entry-level smartphones to supercomputers. Since the explosion of generative AI, demand for ultra-fast memory has surged. AI models require astronomical volumes of data, which must be processed instantly.

This is where what might be called the Sam Altman effect comes into play. In late 2025, to secure its technological lead, OpenAI, backed by massive funding through the Stargate project, signed large-scale contracts with South Korean manufacturers to secure up to 40 percent of global DRAM production for the coming years. The objective was clear: lock in access to components and prevent competitors from keeping up.

This move, as much strategic brilliance as hubris, had a shockwave effect on the market. By capturing such a large share of production, AI giants created an artificial shortage for the rest of the world. Memory manufacturers, sensing an opportunity, redirected their production lines toward high-margin chips for AI servers, neglecting standard components.

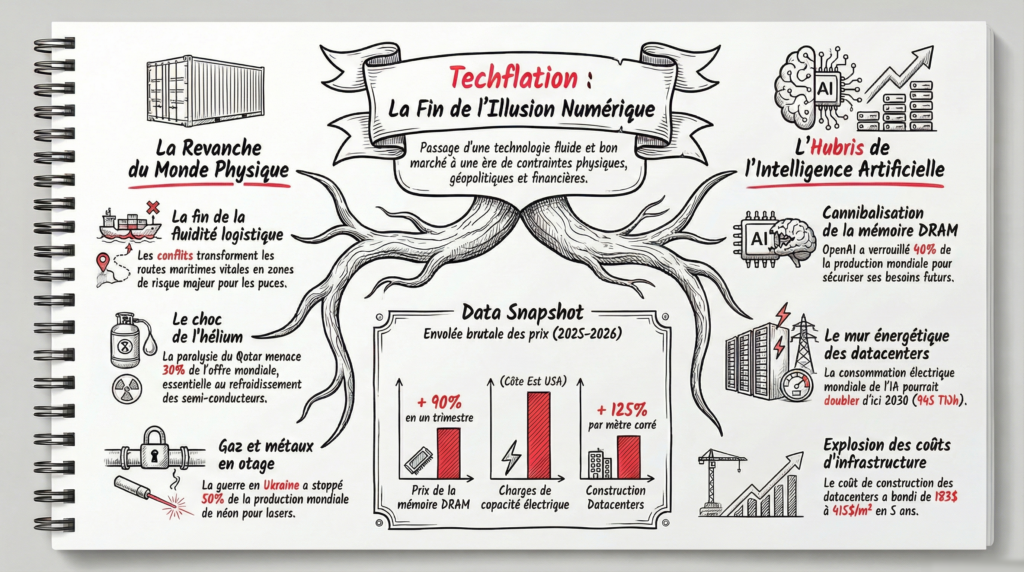

The consequences were immediate. Memory prices for consumer devices saw historic increases. According to TrendForce analysts, contract prices for certain memory products surged by more than 90 percent in a single quarter in early 2026, the largest increase ever recorded [2].

The collateral victims of this war of giants are not other tech giants, but consumers and traditional manufacturers. When memory prices double, the entire economic equation of a student laptop or an affordable smartphone for a worker in Africa collapses. Artificial intelligence, which was supposed to democratize knowledge, is paradoxically making access to basic technology unaffordable for a large part of humanity.

The energy wall, the unsustainable appetite of data centers

To this component crisis is added an even more fundamental physical challenge: energy. Artificial intelligence, far from being immaterial, is an electrical glutton. Training and deploying AI models require massive infrastructures whose energy consumption is exploding.

According to the International Energy Agency, global electricity consumption by data centers could double to reach 945 terawatt-hours by 2030, driven by a 30 percent annual growth in consumption from AI-dedicated servers [15]. In Europe, the Shift Project paints an equally alarming picture: data centers already account for 2.5 percent of total electricity consumption, and this share could double by 2030, even triple by 2035 [16]. In France, where they represent around 2 percent of consumption, demand could quadruple by 2035 [16].

This trajectory is incompatible with decarbonization targets and current electricity production capacities. Tech giants are now forced to invest massively in dedicated energy infrastructures, even considering direct connections between their data centers and nuclear power plants. This energy wall adds enormous inflationary pressure across the entire digital ecosystem, as energy becomes the new bottleneck of innovation.

The concrete consequences are already visible. The cost of building a data center per square meter rose from 183 dollars in 2020 to 415 dollars in 2025, with a projection of 488 dollars for 2026 [22]. On the US East Coast, electricity capacity charges surged by 833 percent between 2025 and 2026 [23]. According to Sightline Climate, which tracks 777 data center projects announced since 2024, between 30 and 50 percent of the capacity planned for this year may not come online on time [24]. For a standard 60 MW AI data center, a six-month delay is enough to reduce the internal rate of return from 17 percent to below 9 percent [29]. The infrastructure bubble is beginning to crack before even reaching full scale.

The perfect storm is therefore here: disrupted trade routes, rare gases in short supply, an industry suffocating itself to feed its AI ambitions, and an energy wall rising before it. While these crises, helium, memory, maritime routes, energy, may at first appear as external and temporary shocks, their repetition and convergence are creating a new structural reality. Techflation emerges precisely from this accumulation of ruptures that transforms a once fluid system into a field of permanent constraints. The consequences of this disastrous alignment will be felt very quickly.

The perfect storm is now in place. The physical foundations of our digital world are shaking under the weight of geopolitics, scarcity and technological hubris. But in concrete terms, what will this disastrous alignment change in your life tomorrow morning? That is what we will explore next week in the second part of this investigation, where we will dive into the shock of reality: rising prices, the Androidcalypse and the end of technological globalization.

References

[1] Fortune / The Associated Press. “Iran war cuts off helium from Qatar, and shortages will start to bite in a few weeks, threatening chip supply chains that fuel the AI boom.” March 21, 2026. https://fortune.com/2026/03/21/iran-war-helium-shortage-qatar-chip-supply-chains-ai-boom/

[2] TrendForce. “Memory Price Outlook for 1Q26 Sharply Upgraded; QoQ Increases of All Product Categories to Hit Record Highs.” February 2, 2026. https://www.trendforce.com/presscenter/news/20260202-12911.html

[5] Fitch Ratings / South China Morning Post. “Korea, Taiwan chip sectors most exposed to helium shortage amid Middle East war.” March 2026. https://www.scmp.com/tech/article/3347005/korea-taiwan-chip-sectors-most-exposed-helium-shortage-amid-middle-east-war-fitch

[6] Phil Kornbluth, Kornbluth Helium Consulting, cited in Scientific American. “The Iran War Disrupts Global Helium Supply and Artificial Intelligence Chip.” March 2026. https://www.scientificamerican.com/article/the-iran-war-disrupts-global-helium-supply-and-artificial-intelligence-chip/

[7] Patrick McGee. Apple in China: The Capture of the World’s Greatest Company. Financial Times / Penguin, 2025.

[8] Reuters. “Russia’s attack on Ukraine halts half of world’s neon output for chips.” March 11, 2022. https://www.reuters.com/technology/exclusive-ukraine-halts-half-worlds-neon-output-chips-clouding-outlook-2022-03-11/

[9] MIT Sloan Management Review. “The Crisis in Ukraine Spells More Trouble for Semiconductor Supply.” May 10, 2022. https://sloanreview.mit.edu/article/russias-invasion-spells-more-trouble-for-semiconductor-supply/

[15] International Energy Agency (IEA). “Energy demand from AI”. 2025. https://www.iea.org/reports/energy-and-ai/energy-demand-from-ai

[16] The Shift Project. “Artificial intelligence, data, computation: what infrastructures in a decarbonized world?”. October 2025. https://theshiftproject.org/publications/intelligence-artificielle-centres-de-donnees-rapport-final/

[22] iRecruit.co. “Data Center Construction Cost Trends 2026”. March 25, 2026. https://www.irecruit.co/insights/data-center-construction-cost-trends-2026

[23] American Action Forum. “Emergency Energy Auction to Prevent Data Center-driven Rate Increases”. January 20, 2026. https://www.americanactionforum.org/insight/emergency-energy-auction-to-prevent-data-center-driven-rate-increases/

[24] Sightline Climate. “Data Center Outlook: Half of 2026 Pipeline May Not Materialize”. February 24, 2026. https://www.sightlineclimate.com/research/data-center-outlook

[26] OECD. “OECD Economic Outlook, Interim Report March 2026: Testing Resilience”. March 2026.

[29] Topp-Mugglestone, Jonas. “Delays in data centre construction cost developers nearly USD15mn per month”. STL Partners, March 27, 2025. https://stlpartners.com/press/delays-in-data-centre-construction/